17 Mar 2023 Morgan Hayze

Swiss Bankers Association Propose The Adoption Of Deposit Token

The release of a white paper by the Swiss Bankers Association highlights the need for Swiss banks to support the development of the country's digital economy. The paper identifies stablecoins as having limited penetration in the Swiss financial system, despite the increasing trend toward end-to-end digitization in business models. Additionally, no Swiss stablecoins are accessible to the general public.

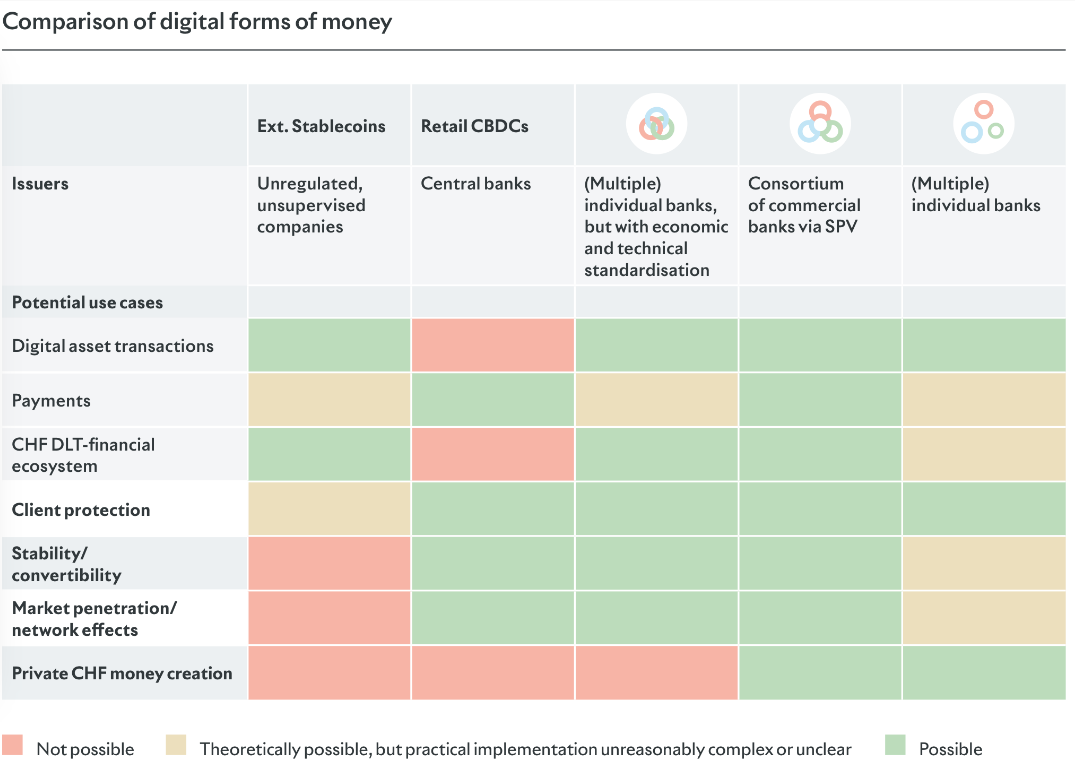

The authors suggest the creation of a deposit token (DT) that is "issued by regulated and adequately supervised intermediaries," redeemed by smart contracts, and denominated in Swiss francs. This deposit token could be designed as a ledger-based security, rather than a set of instructions, to provide it with the greatest potential. The paper identifies three design options for a deposit token: Standardized tokens, colored tokens, and joint tokens. The authors prefer the last choice, which would be issued by a licensed and supervised special-purpose vehicle consisting of participating banks.

Source: SBA

Source: SBA

The DT's fundamental idea came from the "tokenization" of deposits using open-source blockchain technology. The DT is "programmable money," or a completely digital version of the Swiss franc that has programmable functionalities added to it. The primary use cases include decentralized finance applications, payments in the "Economy 4.0" (including payments made between machines inside the Internet of Things), and the trade and settlement of digital assets. The DT's status as a platform technology and a public benefit means that more cutting-edge application areas are likely to develop over time.

A joint deposit token would be flexible, have low fees, and could earn interest when held in bank accounts. It would also be less susceptible to runs than tokens issued by individual banks. The paper indicates that all the economic and legal requirements necessary for the deposit token can be met and that it should ideally operate on a public blockchain with additional protocols for privacy and transaction efficiency. The token would ideally be a layer-2 solution usable in decentralized finance (DeFi) applications and capable of self-custody or bank custody.

Deposit tokens are relatively new to digital currencies, originating in Project Guardian, an initiative launched by the Monetary Authority of Singapore with several financial institutions in May 2022 to explore DeFi applications in wholesale funding markets. JPMorgan, a participant in Project Guardian, executed the first DeFi trade on a public blockchain. JPMorgan and project participant Oliver Wyman released a paper discussing the merits of deposit token technology in February.

Singapore and Project Guardian

The world of digital cash is divided into two camps: traditionalists who want a public authority to provide a safe medium of exchange and experimentalists who believe private money is reliable enough. A new concept has emerged, deposit tokens, which are validated by Singapore's Project Guardian. It involves asset tokenization and programming to trade only against known wallet addresses on a public blockchain. Deposit tokens could make settlement risks go away by reducing fees, settlement times, and counterparty risks. Tokenized deposits, together with CBDCs, may render stablecoins unnecessary, and CBDCs carry the promise of payment by a country's ultimate money-printing authority.

Blockchain central banks token tokens cryptocurrency news crypto news digital asset Banks Stablecoins CBDC Defi Decentralized Finance