31 Mar 2023 Marsha Tusk

The UK To Place Tighter Crypto Regulations In Order To Cut Down Economic Crimes

In an effort to combat economic crime, the government of the United Kingdom has outlined proposals to tighten the regulation of crypto assets.

The U.K. Treasury and Home Office stated in a policy document published on March 30 that they intended to "robustly" regulate cryptocurrency in order to combat its unauthorized usage. The government's economic crime strategy from 2023 to 2026 included an emphasis on legislation as well as combining "the knowledge and capacity of law enforcement agencies" to increase the ability to seize and store crypto assets that are involved in judicial procedures.

“These steps will be in keeping with our ambition to make the U.K. an attractive destination for cryptoassets and cryptoasset innovation in the world,” the policy paper reads, adding that “challenging as it is, effective cryptoasset regulation benefits everyone, including consumers and firms.”

The U.K. government stated in the strategy document that it anticipated criminals to move their cryptocurrency transactions to "less regulated exchanges and services" in other countries. The Financial Conduct Authority, or FCA, of the nation, one of the organizations in charge of enforcing laws governing crypto assets, will collaborate with peers abroad to share information on its response to the regulation and oversight of cryptocurrency. As stated in the paper:

“The [National Crime Agency]’s National Assessment Centre assesses that based on estimates of UK transaction volumes, illicit cryptoasset transactions linked to the UK in 2021 likely equated to at least £1.24 billion (~1% of total transaction value) with a realistic possibility they were significantly higher.”

The government stated that as part of its strategy, it intended to work with several authorities to approve the Economic Crime and Corporate Transparency Law by the end of the fourth quarter of 2023 and apply the Financial Action Task Force's Travel Rule. Additional objectives included enhancing contact with crypto companies by the second quarter of 2024.

While the U.K. appears to be tackling crypto on several fronts, including legislation and law enforcement, taxpayers in the nation have their own reporting requirements. The U.K. Treasury announced in a study published on March 15 that it will modify the self-assessment forms for crypto assets beginning with the 2024–2025 tax year.

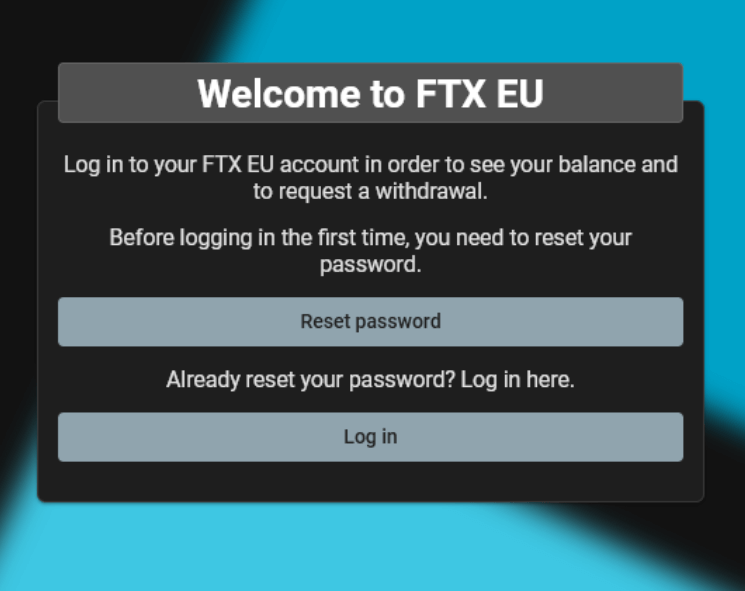

Europeans can now withdraw their cryptos from FTX

Meanwhile, FTX EU, the demised FTX European division, enabled its European customers to file withdrawal requests, via a special website. The move comes almost five months after the global trading platform's bankruptcy and collapses in early November.

According to a report, the Cyprus Securities and Exchange Commission apparently authorized a new website domain.

Source: Twitter

Source: Twitter

“Please be informed that our new domain, www.ftxeurope.eu, has been approved by our regulator CySEC as you have well identified. The website will only be used for all FTX EU LTD clients to be able to claim their FIAT balances. There will be no services or products offered via this website.” the European branch of FTX emailed.

Another subsidiary that has already made reparations to affected clients is FTX Japan. It permitted a total withdrawal of cash in late February that came to around $50 million.

On November 9, just before FTX Group and its 130 related firms (including FTX EU) formally filed for bankruptcy on November 11, the Cyprus regulator asked FTX EU to halt operations.

Cryptocurrency exchange Cryptocurrency Regulations Exchanges News exchange cryptocurrency news crypto news Crypto Assets United Kingdom Regulations